Is Herbalife a pyramid scheme?

No, it is an MLM. Multi-Level-Marketing entity, which is often confused with ‘Pyramid Schemes’. Herbalife Nutrition is a global direct-selling company that has been in existence for more than 40 years and operates in over 90 countries around the globe.

We are going to show you a forensic audit below on historical Herbalife financials, wFe have chosen 2019.

Is Herbalife a pyramid scheme? Summary

ThisF report focuses mainly on the Risk of material misstatement (RMM) in the revenue process. The whole work includes client information collection, ARPs analysis, and expected revenues by regression models. All steps will be very useful in the auditing process on Herbalife Nutrition.

Contents : Is Herbalife a pyramid scheme?

Section I: Introduction & Report Overview 4

Section 2: Initial risk assessment phase activities 4

2.Herbalife’s related history 4

Section 3: Developing Basic ARPs evidence 6

Table 4: Combined horizontal and vertical analysis (part) 6

Section 4: Developing Additional Basic ARPs evidence 7

1.Plots of the “audited” quarterly sales 7

Graph 1: Quarterly sales of Herbalife (audited) 8

Section 5: Developing and Interpreting Advanced ARPs evidence concerning auditor expectations 9

Graph 2: Auditor’s expectation for 2019 10

Table 7: Auditor’s expectation for 2019 10

Graph 3: Auditor’s expectation for 2019 11

Table 9: Auditor’s expectation for 2019 11

4.Multiple regression model with trend and some economic indices 12

Graph 4: Auditor’s expectation for 2019 13

Table 11: Auditor’s expectation for 2019 13

Section 6: Summary and Main Audit Conclusions 13

Key Audlish and Statlish terms 15

Section I: Introduction & Report Overview

1.Purpose

The purpose of every section is to provide useful information in the risk assessment phase. In section 2, we collect materials about Herbalife to help auditors understand the client. In sections 3 and 4, the focus is to gather tables we need and show the financial conditions and revenue situations of Herbalife in the recent three years. Through analyzing these data, we can decide the transactions and accounts at the risk of material misstatements in the revenue process. Then, we can select appropriate substantive test procedures to apply in the auditing process. In section 5, we will make use of a simple regression model and multiple regression models to analyze and predict sales revenues of Herbalife in 2019. By comparing these models, auditors can choose the best model to analyze Herbalife’s sales.

2.Key Audit Findings

1. Herbalife’s potential inherent risks

2. Herbalife’s financial and sales revenue conditions.

3. Herbalife’s risk of overstatement of sales revenue in 2019.

Section 2: Initial risk assessment phase activities

1.Herbalife information

Herbalife Nutrition is a global nutrition company whose purpose is to make the world healthier and happier. Together with independent distributors, Herbalife Nutrition is committed to providing solutions to the worldwide problems of poor nutrition and obesity, an aging population, sky-rocketing public healthcare costs, and a rise in entrepreneurs of all ages. Herbalife Nutrition offers high-quality, science-backed products, most of which are produced in Company-operated facilities, one-on-one coaching with an independent distributor, and a supportive community approach that inspires customers to embrace a healthier, more active lifestyle.

Herbalife Nutrition has over 8,000 employees worldwide and is traded on the New York Stock Exchange (NYSE: HLF). (https://company.herbalife.com/)

2.Herbalife’s related history

In recent years, Herbalife has issued some notes and taken use of many credit facilities as a kind of financing method, which involves some complicated transactions. On February 15, 2017, Herbalife entered into a $1,450.0 million senior secured credit facility. On August 16, 2018, the company entered into a new $1.25 billion senior secured credit facility. In February 2014, Herbalife issued a $1.15 billion aggregate principal amount of convertible senior notes. In March 2018, Herbalife issued a $550 million aggregate principal of new convertible senior notes due 2024.

In addition, in the prior three years, the sales of products of Herbalife show an obvious fluctuation. From 2016 to 2017, Herbalife shows a slight decrease in sales revenue. However, from 2017 to 2018, the sales revenue of the corporation increases more than 10% which is material.

3.Industry insight

Herbalife Nutrition files under SIC code 5122: WHOLESALE-DRUGS PROPRIETARIES & DRUGGISTS’ SUNDRIES. The industry is full of competition and full of opportunities. The global dietary supplements market size was estimated at USD 115.06 billion in 2018. The global weight loss & weight management market is expected to reach USD 264.68 billion by 2025 growing at a CAGR of 5.3% over the study period.

4.Potential Inherent Risks

- “Complexity of revenue recognition” is a factor that could increase inherent risk. Because of multiple-level marketing, Herbalife distributes products exclusively to and through independent Members, and Herbalife depends upon them directly for substantially all of its sales. Accordingly, Herbalife’s revenue recognition depends in significant part upon sales Members. Cheating from Members for any reason could negatively impact revenue recognition of the products. (Herbalife Nutrition, 2018)

- “Complicated transactions in financing activities” is also an important point. Herbalife repurchases shares amounted to approximately $4.5 billion. To achieve it, Herbalife uses many ways to finance such as convertible senior notes in 2014, a senior secured credit facility in 2018, which will put a huge impact on long-term liabilities and current liabilities accounts. Huge debt financing increases the inherent risk of Herbalife. At the same time, there may be some debt covenants between Herbalife and some financial institutes which may lead to financial misstatement.

5.Section 2 assessment

In the section, “Complexity of revenue recognition” and “Complicated transactions in financing activities” are two factors that may increase RMM. So, we should pay attention to them.

Quantitative assessment in the section (from 0.00 to 1.00) of RMM is as following:

IR=0.25

CR=0.05

RMM=0.0125

Section 3: Developing Basic ARPs evidence

1.Risks of WCGW

In the net sales section, the primary risk of material misstatements will exist in the transaction of Recording sales. Any adjustment in the section will lead to an overstatement or understatement of revenue. In the appendix, table1, 2, 3 show the Balance Sheet, Income statement, and Cash Flow Statement for three prior years. According to table 4, the combined horizontal and vertical analysis, Herbalife suffers from a depression in 2017 in net sales, but it gets a significant increase in 2018. Pressure to achieve higher net sales and sudden increment may create a risk of material misstatements.

Table 4: Combined horizontal and vertical analysis (part)

| 2018 (BASE YEAR) | % of Sales | Diff with base year | % change | 2017 | % of Sales | Diff with base year | % change | 2016 | % of Sales | |

| Net sales | 4,891.80 | 100.00% | 464.10 | 10.48% | 4,427.70 | 100.00% | -60.70 | -1.35% | 4,488.40 | 100.00% |

| Cost of sales | 919.30 | 18.79% | 70.70 | 8.33% | 848.60 | 19.17% | -6.00 | -0.70% | 854.60 | 19.04% |

| Gross profit | 3,972.50 | 81.21% | 393.40 | 10.99% | 3,579.10 | 80.83% | -54.70 | -1.51% | 3,633.80 | 80.96% |

The process of recording sales involves preparing and sending prenumbered sales invoices to customers (billing customers) and recording sales invoices accurately and in the proper accounting period (recording sales). The auditor’s primary concerns regarding recording sales are that sales invoices are recorded accurately and in the proper period. The latter pertains to when the revenue is earned, which is usually when the goods are shipped. The auditor’s primary concerns regarding billing are that customers are billed (1) for all shipments, (2) only for actual shipments (no duplicate billings or fictitious transactions), and (3) at authorized prices.

Risks of WCGW will potentially exist in:

1. Some shipments may not be billed.

2. Billing may be made for fictitious transactions, or duplicate billing may be made.

3. Sales invoices may be recorded in the incorrect accounting period.

4. Sales invoices may be recorded in the incorrect amount (incorrect quantities or prices).

5. Invoices may not be journalized or posted to customer accounts.

6. Sales invoices may be billed to the wrong customer.

7. Customers may be billed incorrect amounts.

2.The specific assertions

The specific assertions that concern me include Occurrence, Accuracy, Cutoff, Existence, Valuation, and allocation.

1. Occurrence and Existence assertions show us that the transactions and account balances are existing. They require that documents such as sales invoices, shipping documents, and sales orders match the record in accounts or accounting systems.

Potential misstatements include that billing may be made for fictitious transactions, or duplicate billing may be made.

2. Cutoff and Allocation assertions mean that every transaction is recorded in the right period of time and for the right transactions or events. Recording revenue prematurely will make revenue overstated, vice versa.

Potential misstatements include sales invoices that may be recorded in the incorrect accounting period.

3. Accuracy and Valuation assertions need transactions to be recorded in the right amount and to the right customers.

Potential misstatements include sales invoices that may be recorded in the incorrect amount (incorrect quantities or prices), Sales invoices may be billed to the wrong customer and Customers may be billed incorrect amounts.

3.Section 3 assessment

The section, “Occurrence, Accuracy, Cutoff, Existence, Valuation, and allocation” are assertions that may influence RMM. Therefore, auditors should pay attention to them.

Section 4: Developing Additional Basic ARPs evidence

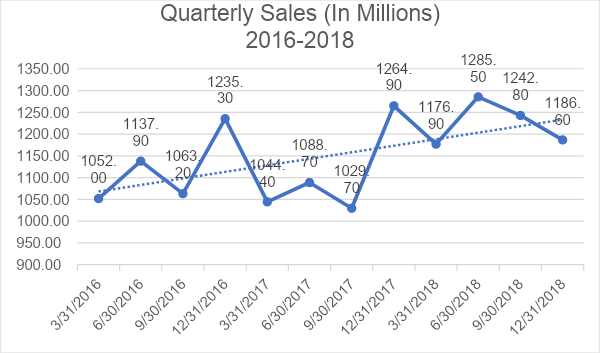

1.Plots of the “audited” quarterly sales

According to graph 1, auditors can get following conclusions:

- According to the data of these three years, the average sale of 2018 is higher than that of 2017 and 2016. Therefore, the quarterly sales have a trend of increasing.

- In 2016 and 2017, the sales in every season show a seasonal pattern regardless of some slight differences which are not obvious in sales data in 2018.

- In 2016 and 2017, the company will have an exceptional sales increase in the final quarter. But it did not happen in the fourth quarter of 2018.

Graph 1: Quarterly sales of Herbalife (audited)

2.Substantive tests

The substantive tests the audit team would need to complete include:

a) In tests of details of transactions:

- Vouch recorded revenue transactions to support sales invoices, shipping documents, and sales orders.

- Select a sample of recorded sales transactions from several days before and after year-end and examine supporting sales invoices and shipping documents to determine sales were recorded in the proper period.

b) In tests of details of balances:

- Confirm accounts receivable.

a. Determine the form, timing, and extent of confirmation requests.

b. Select and execute samples and investigate exceptions.

c. For positive confirmation requests for which no reply was received, perform alternative follow-up procedures: Vouch items comprising balance at confirmation date to documentary support such as sale orders and shipping documents.

3.Forecasting of revenue

According to tables 4 and 5, the unaudited average quarterly sale of 2019 seems reasonable and acceptable, and the unaudited average receivable which is slightly higher than prior years is also plausible. Therefore, in this aspect, there is no obvious risk of data being overstated or understated.

| 2019 | 2018 | 2017 | 2016 | |

| Average Quarterly Sale (In Millions) | 1,218.93 | 1,222.95 | 1,106.93 | 1,122.10 |

4.Section 4 assessment

In the section, fluctuation of sales revenue in 2018 may increase the uncertainty of revenue expectation. Therefore, more substantive procedures should be put on sales recognition.

Section 5: Developing and Interpreting Advanced ARPs evidence concerning auditor expectations

1.Introduction

In this section, I will introduce a simple regression model and two multiple regression models to develop Auditor’s Expectation concerning Revenues. I will make use of revenue data from 2016 to 2018 as inputs to create these regression models. Then, according to the summary output, we can create an equation on Herbalife’s revenue and predict its revenue situation for 2019. Finally, I will analyze the difference between expectations and real figures and choose the best model.

2.Simple regression model

According to data from Table 5, we can get quarterly sales of Herbalife from 2016 to 2018 and make use of this data to make a simple regression model. The summary of data is shown in table 6 in the appendix.

Estimated model equation:

Sales revenue[hat]=1053+15 Quarter

| Quarters of 2019 | Expectation (in million) | |

| Spring | 1248 | |

| Summer | 1263 | |

| Fall | 1278 | |

| Winter | 1293 | |

| Total 2019 revenue | $ 5082 |

The simple regression indicates a linear relationship between quarters and sales revenue of Herbalife. The estimated model equation is Sales revenue[hat]=1053+15 Quarter as shown in graph 2, it represents that each quarter, Herbalife’s sales revenue is expected to increase by $15 million. By using the equation, we can get that our auditor’s expected total sales revenue for 2019 is $5082 million. In addition, the significant F and P-value is 0.0487, which means that both simple regressions and independent variables are statistically significant. However, R square is only 0.3348, which means only 33.48% of data fits the simple regression model.

Graph 2: Auditor’s expectation for 2019

According to table 7, comparing the asserted sales revenue and auditor’s expectation, the asserted total sales revenues for the first three quarters is $189.45 million less than the simple regression model expected, 3.49% difference. Auditors set a 5% difference as materiality. Therefore, there is a possibility that Herbalife understated the sales revenue. But we cannot say that the company has material misstatement because 3.49% is not very close to the 5% that the auditor can accept. However, spring data is more than a 5% difference, so we should pay more attention to the season.

Table 7: Auditor’s expectation for 2019

| Auditor’s Expectations for 2019 Quarterly Sales Revenue of Herbalife.(in million) | |||||||

| Sales revenue[hat]=1053+15 Quarter | |||||||

| $ | $ | % | |||||

| Quarters | Quarter | Asserted | Expectation | Difference | Materiality | Materiality | Difference |

| Spring | 13 | $ 1172.2 | $ 1248 | ($ 75.8) | $ 62.4 | 5% | -6.07% |

| Summer | 14 | $ 1240.1 | $ 1263 | ($ 22.9) | $ 63.15 | 5% | -1.81% |

| Fall | 15 | $ 1244.5 | $ 1278 | ($ 33.5) | $ 63.9 | 5% | -2.62% |

| Winter | 16 | – | – | – | – | 5% | – |

| Total 2019 revenue | $ 3656.8 | $ 3789 | ($132.2) | $ 189.45 | 5% | -3.49% |

3.Multiple regression model with summer, fall, winter, and trend variables and its Discussion & Evaluation

In this regression model, I choose season variables as dummy variables of the model and take the spring variable away because the other three seasons show more influence on the prediction of revenue. The summary of data is shown in table 7 in the appendix.

Estimated model equation:

Sales revenue[hat]=1028+12.6 Quarter+67 Summer-4.41 Fall+100 Winter

| Quarters of 2019 | Expectation (in million) | |

| Spring | 1191.8 | |

| Summer | 1271.4 | |

| Fall | 1212.6 | |

| Winter | 1329.6 | |

| Total 2019 revenue | $ 5005.4 |

The multiple regressions indicate a linear relationship between all four seasons and the sales revenue of Herbalife. The estimated model equation is Sales revenue[hat]=1028+ 12.6 Quarter+ 67 Summer- 4.41 Fall 100 Winter as shown in graph 3, it represents that each quarter Herbalife’s sales revenue is expected to increase $13.09 million. For Spring, the equation can simplify to Sales revenue[hat]= 1028+ 12.6 Quarter; for summer, Sales revenue[hat]= 1028+ 12.6 Quarter 67 Summer; for fall, Sales revenue[hat]=1028+12.6 Quarter-4.41 Fall; for winter, Sales revenue[hat]=1028+12.6 Quarter+100 Winter. By using the equation, we can get our auditor’s expected total sales revenue for 2019 to be $5005.4 million. Moreover, the significant F-value is 0.15, which means that the regression model is not statistically significant and satisfactory but is also acceptable. The P-value for independent variables for the quarter, summer, and winter is 0.105, 0.322, 0.172, which are also not statistically significant. In particular, the P-value for independent variables for fall is too high. Also, R square is 57.3%, which means 57.3% of the data fits the multivariate dummy variables model.

Graph 3: Auditor’s expectation for 2019

Comparing the asserted sales revenue and auditor’s expectation in table 9, auditors can find that the asserted total sales revenues for the first three quarters are only $19 million less than the multiple regression model expected, 0.52% difference. Auditors set a 5% difference as materiality. Therefore, there seems to be almost no possibility that Herbalife misstated the sales revenue. However, the difference between summer and fall sales is near 5%. Auditors should pay more attention to figure out the reasons leading to the fluctuation.

Table 9: Auditor’s expectation for 2019

| Auditor’s Expectations for 2019 Quarterly Sales Revenue of Herbalife. | |||||||

| (in million) | |||||||

| Sales revenue[hat]=1028+12.6 Quarter+67 Summer-4.41 Fall+100 Winter | |||||||

| Quarters | Quarter | Asserted | Expectation | Difference | Materiality | Materiality | Difference |

| Spring | 13 | $1,172.20 | $1,191.80 | ($19.60) | $59.59 | 5% | -1.64% |

| Summer | 14 | $1,240.10 | $1,271.40 | ($31.30) | $63.57 | 5% | -2.46% |

| Fall | 15 | $1,244.50 | $1,212.60 | $31.90 | $60.63 | 5% | 2.63% |

| Winter | 16 | – | – | – | – | 5% | – |

| Total 2015 revenue | $3,656.80 | $3,676 | ($19.00) | $183.79 | 5% | -0.52% |

4.Multiple regression model with trend and some economic indices

I also try to use some economic indices as independent variables to find the relationship between Herbalife’s sales and these economic indices, which is exhibited in table 10. In the regression, I use DP Income, Retail Sales, and S&P 500 as economic variables. For DP Income and Retail Sales, I choose the average value per season; for S&P 500, I choose the data of the last day per season.

Estimated model equation:

Sales revenue[hat]=-8321+0.526 DPIncome+0.004 Retail Sales+0.34 S&P 500 -133.2 Trend

| Quarters of 2019 | Expectation (in million) | |

| Spring | 1060.5 | |

| Summer | 1224.9 | |

| Fall | 1203.2 | |

| Winter | – | |

| First three-reasons revenue | $ 3488.6 |

The multiple regressions indicate a linear relationship between some economic figures and sales revenue of Herbalife. The estimated model equation is Sales revenue[hat]=-8321+0.526 DPIncome+0.004 Retail Sales+0.34 S&P 500 -133.2 Trend as shown in graph 4. By using the equation, the auditor’s expected sales revenue for the first three seasons of 2019 is $3488.6 million. Moreover, the significant F-value is 0.0097, which means that the regression model is very statistically significant. The P-value for independent variables for DP Income, Retail Sales, S&P 500, and trend are 0.0336, 0.00515, 0.0371, 0.0204, which are also very statistically significant. Therefore, figures from the model are very reliable to auditors. Also, R square is 81.91%, which means 81.91% of data fits the multivariate dummy variables model.

Graph 4: Auditor’s expectation for 2019

Table 11 shows us that the asserted total sales revenues for the first three quarters are $168.2 million more than the multiple regression model expected, a total 4.82% difference. Auditors set a 5% difference as materiality. Therefore, there seems to be a possibility that Herbalife overstated the sales revenue because 4.82% is very close to 5%. In addition, the difference in spring is more than 10% which is extremely significant and the difference in fall is also significant. Auditors must pay more effort on these two seasons to make sure the financial reports are prepared properly.

Table 11: Auditor’s expectation for 2019

| Auditor’s Expectations for 2019 Quarterly Sales Revenue of Herbalife. | |||||||

| (in million) | |||||||

| Sales revenue[hat]=1053+15 Quarter | |||||||

| Quarters | Quarter | Asserted | Expectation | Difference | Materiality | Materiality | Difference |

| Spring | 13 | $1,172.20 | $1,060.50 | $111.70 | $53.03 | 5% | 10.53% |

| Summer | 14 | $1,240.10 | $1,224.90 | $15.20 | $61.25 | 5% | 1.24% |

| Fall | 15 | $1,244.50 | $1,203.20 | $41.30 | $60.16 | 5% | 3.43% |

| Winter | 16 | – | – | – | – | 5% | – |

| Total 2015 revenue | $3,656.80 | $3,489 | $168.20 | $174.43 | 5% | 4.82% |

Section 5 assessment

In the section, by using several regression models, we choose the multiple regression model with trend and some economic indices as the best one, which tells us the corporate has a risk of overstatement, especially spring and fall. Therefore, more efforts should be put into this section.

Section 6: Summary and Main Audit Conclusions

In the report, we focus on the risk assessment phase of auditing. In section 2, we collect basic information on Herbalife and its industry. At the same time, we point out the inherent risks the company has, which are “Complexity of revenue recognition” and “Complicated transactions in financing activities”.

In sections 3 and 4, we pay more attention to ARP analysis. By analyzing the financial data of Herbalife in recent years. We found some assertions that we should study more and make a plan for substantive tests. The specific assertions that concern me include Occurrence, Accuracy, Cutoff, Existence, Valuation, and allocation. Procedures we can use include “Vouch recorded revenue transactions to supporting sales invoices, shipping documents, and sales orders; select a sample of recorded sales transactions from several days before and after year-end and examine supporting sales invoices and shipping documents to determine sales were recorded in the proper period; confirm accounts receivable.”

In section 5, we make use of some regression models to predict Herbalife’s sales revenue and compare them with assorted figures. Comparing these models, we think the Multiple regression model with trend and some economic indices is the best. The model has a higher R square and most statistically significant than other models. At the same time, it utilizes many vital economic indices which make the model more reliable. Therefore, this model will help predict future sales revenue. By using the model, we can get the conclusion that there is a possibility of overstatement in the sales of Herbalife. The asserted total sales revenues for the first three quarters is $168.2 million more than the multiple regression model expected, a total 4.82% difference. In addition, we should put more effort into auditing materials from spring and fall.

References

- https://www.sec.gov/Archives/edgar/data/1180262/000156459019003287/hlf-10k_20181231.htm. 10-K (2018)

- https://www.sec.gov/Archives/edgar/data/1180262/000156459018002880/0001564590-18-002880-index.htm. 10-K (2017)

- Auditing A Practical Approach with Data Analytics. [2019], LAURA D. WILEY, RAYMOND N. JOHNSON.

- https://finance.yahoo.com/quote/%5EGSPC/history?period1=1451577600&period2=1483977600&interval=1d&filter=history&frequency=1d

- https://www.census.gov/searchresults.html?q=Retail+Sales&page=1&stateGeo=none&searchtype=web&cssp=SERP&_charset_=UTF-8

- https://www.globenewswire.com/newsrelease/2019/06/06/1865134/0/en/Weight-Loss-and-Weight-Management-Market-will-grow-at-a-CAGR-of-5-3-to-hit-264-68-Bn-by-2025-Adroit-Market-Research.html. Weight Loss and Weight Management Market will grow at a CAGR of 5.3% to hit $264.68 Bn by 2025 – Adroit Market Research.

- https://www.macrotrends.net/stocks/charts/HLF/herbalife/debt-equity-ratio. Herbalife Debt to Equity Ratio 2006-2019.

- http://fernfortuniversity.com/term-papers/swot/nyse/681-herbalife-ltd-.php. Herbalife Ltd. SWOT Analysis / Matrix.

- “Herbalife Will Restructure Its Multi-level Marketing Operations and Pay $200 Million For Consumer Redress to Settle FTC Charges”. Federal Trade Commission. 2016-07-15. Retrieved 2018-05-09.

- “What is Herbalife?”. Discover Good Nutrition, Fitness & Beauty. Herbalife. Retrieved June 8, 2017.

Key Audit and Statlish terms

- RMM: The risk of material misstatement is the risk that the financial statements of an organization have been misstated to a material degree.

- Audit risk: Audit risk is the risk that an auditor expresses an inappropriate audit opinion when financial statements are materially misstated.

- Fraud: An intentional act through the use of deception that results in a misstatement in financial statements that are the subject of an audit.

- Dummy Variable: A dummy variable is a numerical variable used in regression analysis to represent subgroups of the sample in study.

- Regression analysis: In statistical modeling, regression analysis is a set of statistical processes for estimating the relationships between a dependent variable (often called the ‘outcome variable’) and one or more independent variables (often called ‘predictors’, ‘covariates’, or ‘features’).

Appendix

Table 1: The three prior years of audited B/S data

| HERBALIFE NUTRITION LTD. AND SUBSIDIARIES | |||

| CONSOLIDATED BALANCE SHEETS | |||

| (in millions, except share and par value amounts) | |||

| December 31, 2018 | December 31, 2017 | December 31, 2016 | |

| ASSETS | |||

| CURRENT ASSETS: | |||

| Cash and cash equivalents | 1,198.90 | 1,278.80 | 844 |

| Receivables, net of allowance for doubtful accounts | 70.5 | 93.3 | 70.3 |

| Inventories | 381.8 | 341.2 | 371.3 |

| Prepaid expenses and other current assets | 153.8 | 147 | 176.9 |

| Total current assets | 1,805.00 | 1,860.30 | 1,462.50 |

| Property, plant, and equipment, at cost, net of accumulated depreciation and amortization | 360 | 377.5 | 378 |

| Marketing-related intangibles and other intangible assets, net | 310.1 | 310.1 | 310.1 |

| Goodwill | 92.9 | 96.9 | 89.9 |

| Other assets | 221.8 | 250.3 | 324.9 |

| Total assets | 2,789.80 | 2,895.10 | 2,565.40 |

| LIABILITIES AND SHAREHOLDERS’ DEFICIT | |||

| CURRENT LIABILITIES: | |||

| Accounts payable | 81.1 | 67.8 | 66 |

| Royalty overrides | 281.4 | 277.7 | 261.2 |

| Current portion of long-term debt | 678.9 | 102.4 | 9.5 |

| Other current liabilities | 547.4 | 458.9 | 454.8 |

| Total current liabilities | 1,588.80 | 906.8 | 791.5 |

| NON-CURRENT LIABILITIES: | |||

| Long-term debt, net of current portion | 1,774.90 | 2,165.70 | 1,438.40 |

| Other non-current liabilities | 149.5 | 157.3 | 139.2 |

| Total liabilities | 3,513.20 | 3,229.80 | 2,369.10 |

| COMMITMENTS AND CONTINGENCIES | |||

| SHAREHOLDERS’ (DEFICIT) EQUITY: | |||

| Common shares, $0.0005 par value; 2.0 billion shares authorized; 142.8 million (2018), 164.7 million (2017) shares outstanding and 186.2 million (2016) shares outstanding | 0.1 | 0.1 | 0.1 |

| Paid-in capital in excess of par value | 341.5 | 407.3 | 467.6 |

| Accumulated other comprehensive loss | -209.8 | -165.4 | -205.1 |

| Accumulated deficit | -526.3 | -248.1 | -66.3 |

| Treasury stock, at cost, 10.0 million (2018) and 10.0 million (2017) shares | -328.9 | -328.6 | |

| Total shareholders’ deficit | -723.4 | -334.7 | 196.3 |

| Total liabilities and shareholders’ deficit | 2,789.80 | 2,895.10 | 2,565.40 |

Table 2: The three prior years of audited I/S data

| HERBALIFE NUTRITION LTD. AND SUBSIDIARIES | |||

| CONSOLIDATED STATEMENTS OF INCOME | |||

| (in millions, except share and par value amounts) | |||

| Year Ended December 31, | |||

| 2018 | 2017 | 2016 | |

| Net sales | 4,891.80 | 4,427.70 | 4,488.40 |

| Cost of sales | 919.30 | 848.60 | 854.60 |

| Gross profit | 3,972.50 | 3,579.10 | 3,633.80 |

| Royalty overrides | 1,364.00 | 1,254.20 | 1,272.60 |

| Selling, general, and administrative expenses | 1,955.20 | 1,758.60 | 1,966.90 |

| Other operating income | -29.8 | -50.8 | -63.8 |

| Operating income | 683.1 | 617.1 | 458.1 |

| Interest expense | 181 | 160.8 | 99.3 |

| Interest income | 19.4 | 14.5 | 5.9 |

| Other expense (income), net | 57.3 | -0.4 | — |

| Income before income taxes | 464.2 | 471.2 | 364.7 |

| Income taxes | 167.6 | 257.3 | 104.7 |

| NET INCOME | 296.6 | 213.9 | 260 |

| Earnings per share: | |||

| Basic | 2.12 | 1.35 | 1.57 |

| Diluted | 1.98 | 1.29 | 1.51 |

| Weighted-average shares outstanding: | |||

| Basic | 140.2 | 158.5 | 166.1 |

| Diluted | 149.5 | 165.7 | 172.2 |

Table 3: The three prior years of audited cash flow data

| HERBALIFE NUTRITION LTD. AND SUBSIDIARIES | |||

| CONSOLIDATED STATEMENTS OF CASH FLOWS | |||

| (in millions) | |||

| Year Ended December 31, | |||

| 2018 | 2017 | 2016 | |

| Cash flows from operating activities: | |||

| Net income | 296.6 | 213.9 | 260 |

| Adjustments to reconcile net income to net cash provided by operating activities: | |||

| Depreciation and amortization | 100.4 | 99.8 | 98.3 |

| Share-based compensation expenses | 35.5 | 42.1 | 40.2 |

| Non-cash interest expense | 63.8 | 60.2 | 55.7 |

| Deferred income taxes | -8.1 | 97.8 | -36.4 |

| Inventory write-downs | 17.4 | 20.7 | 15.8 |

| Foreign exchange transaction loss | 8 | 2.4 | 3.7 |

| Loss on extinguishment of debt | 48.5 | — | — |

| Other | 7.1 | 1.9 | -11.7 |

| Changes in operating assets and liabilities: | |||

| Receivables | 2.8 | -22.2 | — |

| Inventories | -83.3 | 37.9 | -71.6 |

| Prepaid expenses and other current assets | -5.1 | 38.3 | 0.8 |

| Accounts payable | 21.7 | -5 | -1.3 |

| Royalty overrides | 22.8 | 6 | 20.9 |

| Other current liabilities | 106.8 | -17.1 | 12.4 |

| Other | 13.5 | 14.1 | -19.5 |

| Net cash provided by operating activities | 648.4 | 590.8 | 367.3 |

| Cash flows from investing activities: | |||

| Purchases of property, plant, and equipment | -84 | -95.5 | -143.4 |

| Other | 0.1 | 0.3 | 1 |

| Net cash used in investing activities | -83.9 | -95.2 | -142.4 |

| Cash flows from financing activities: | |||

| Borrowings from senior secured credit facility, net of discount | 998.1 | 1,274.00 | 200 |

| Principal payments on senior secured credit facility and other debt | -1,237.40 | -494.5 | -438.8 |

| Proceeds from convertible senior notes | 550 | — | — |

| Repurchase of convertible senior notes | -582.5 | — | — |

| Proceeds from senior notes | 400 | — | — |

| Debt issuance costs | -29.9 | -22.6 | — |

| Share repurchases | -750.3 | -844.2 | -13.2 |

| Proceeds from settlement of capped call transactions | 55.9 | — | — |

| Other | 3 | 2.1 | -0.3 |

| Net cash used in financing activities | -593.1 | -85.2 | -252.3 |

| Effect of exchange rate changes on cash, cash equivalents, and restricted cash | -51.9 | 28.2 | -20.1 |

| Net change in cash, cash equivalents, and restricted cash | -80.5 | 438.6 | -47.5 |

| Cash, cash equivalents, and restricted cash, beginning of period | 1,295.50 | 856.9 | 904.4 |

| Cash, cash equivalents, and restricted cash, end of period | 1,215.00 | 1,295.50 | 856.9 |

| Cash paid during the year: | |||

| Interest paid | 106.1 | 100.7 | 45.4 |

| Income taxes paid | 158.9 | 158.8 | 162.9 |

Table 4: Combined horizontal and vertical analysis

| HERBALIFE NUTRITION LTD. AND SUBSIDIARIES | ||||||||||

| CONSOLIDATED STATEMENTS OF INCOME | ||||||||||

| (in millions, except share and par value amounts) | ||||||||||

| Year Ended December 31, | ||||||||||

| 2018 (BASE YEAR) | % of Sales | Diff with base year | % change | 2017 | % of Sales | Diff with base year | % change | 2016 | % of Sales | |

| Net sales | 4,891.80 | 100.00% | 464.10 | 10.48% | 4,427.70 | 100.00% | -60.70 | -1.35% | 4,488.40 | 100.00% |

| Cost of sales | 919.30 | 18.79% | 70.70 | 8.33% | 848.60 | 19.17% | -6.00 | -0.70% | 854.60 | 19.04% |

| Gross profit | 3,972.50 | 81.21% | 393.40 | 10.99% | 3,579.10 | 80.83% | -54.70 | -1.51% | 3,633.80 | 80.96% |

| Royalty overrides | 1,364.00 | 27.88% | 109.80 | 8.75% | 1,254.20 | 28.33% | -18.40 | -1.45% | 1,272.60 | 28.35% |

| Selling, general, and administrative expenses | 1,955.20 | 39.97% | 196.60 | 11.18% | 1,758.60 | 39.72% | -208.30 | -10.59% | 1,966.90 | 43.82% |

| Other operating income | -29.8 | -0.61% | 21.00 | -41.34% | -50.8 | -1.15% | 13.00 | -20.38% | -63.8 | -1.42% |

| Operating income | 683.1 | 13.96% | 66.00 | 10.70% | 617.1 | 13.94% | 159.00 | 34.71% | 458.1 | 10.21% |

| Interest expense | 181 | 3.70% | 20.20 | 12.56% | 160.8 | 3.63% | 61.50 | 61.93% | 99.3 | 2.21% |

| Interest income | 19.4 | 0.40% | 4.90 | 33.79% | 14.5 | 0.33% | 8.60 | 145.76% | 5.9 | 0.13% |

| Other expense (income), net | 57.3 | 1.17% | 57.70 | -14425.00% | -0.4 | -0.01% | N/A | N/A | — | 0.00% |

| Income before income taxes | 464.2 | 9.49% | -7.00 | -1.49% | 471.2 | 10.64% | 106.50 | 29.20% | 364.7 | 8.13% |

| Income taxes | 167.6 | 3.43% | -89.70 | -34.86% | 257.3 | 5.81% | 152.60 | 145.75% | 104.7 | 2.33% |

| NET INCOME | 296.6 | 6.06% | 82.70 | 38.66% | 213.9 | 4.83% | -46.10 | -17.73% | 260 | 5.79% |

Table 5: Quarterly sales of Herbalife

| Period of Report | Quarterly Sales (In Millions) | |

| 2019-9-30 | 1,244.50 | (unaudited) |

| 2019-6-30 | 1,240.10 | (unaudited) |

| 2019-3-31 | 1,172.20 | (unaudited) |

| 2018-12-31 | 1,186.60 | |

| 2018-9-30 | 1,242.80 | |

| 2018-6-30 | 1,285.50 | |

| 2018-3-31 | 1,176.90 | |

| 2017-12-31 | 1,264.90 | |

| 2017-9-30 | 1,029.70 | |

| 2017-6-30 | 1,088.70 | |

| 2017-3-31 | 1,044.40 | |

| 2016-12-31 | 1,235.30 | |

| 2016-9-30 | 1,063.20 | |

| 2016-6-30 | 1,137.90 | |

| 2016-3-31 | 1,052.00 |

Table 6: Summary output of Herbalife’s simple regression model

| SUMMARY OUTPUT | ||||||

| Regression Statistics | ||||||

| Multiple R | 0.578578295 | |||||

| R Square | 0.334752844 | |||||

| Adjusted R Square | 0.268228128 | |||||

| St Error | 79.98715285 | |||||

| Observations | 12 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 1 | 32194.50295 | 32194.50295 | 5.032007131 | 0.048737774 | |

| Residual | 10 | 63979.44621 | 6397.944621 | |||

| Total | 11 | 96173.94917 | ||||

| Coefficients | St Error | t Stat | P-value | Lower 95% | Upper 95% | |

| Intercept | 1053.128788 | 49.22868952 | 21.39258222 | 1.11029E-09 | 943.4404321 | 1162.817144 |

| Quarter | 15.00454545 | 6.688861747 | 2.243213572 | 0.048737774 | 0.100832719 | 29.90825819 |

Table 7: Auditor’s expectation for 2019

| Auditor’s Expectations for 2019 Quarterly Sales Revenue of Herbalife.(in million) | |||||||

| Sales revenue[hat]=1053+15 Quarter | |||||||

| $ | $ | % | |||||

| Quarters | Quarter | Asserted | Expectation | Difference | Materiality | Materiality | Difference |

| Spring | 13 | $ 1172.2 | $ 1248 | ($ 75.8) | $ 62.4 | 5% | -6.07% |

| Summer | 14 | $ 1240.1 | $ 1263 | ($ 22.9) | $ 63.15 | 5% | -1.81% |

| Fall | 15 | $ 1244.5 | $ 1278 | ($ 33.5) | $ 63.9 | 5% | -2.62% |

| Winter | 16 | – | – | – | – | 5% | – |

| Total 2019 revenue | $ 3656.8 | $ 3789 | ($132.2) | $ 189.45 | 5% | -3.49% |

Table 8: Multivariate Dummy Variables Model (summer, fall, winter and Trend Variables)

| SUMMARY OUTPUT | ||||||

| Regression Statistics | ||||||

| Multiple R | 0.756747238 | |||||

| R Square | 0.572666382 | |||||

| Adjusted R Square | 0.328475743 | |||||

| St Error | 76.62372037 | |||||

| Observations | 12 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 4 | 55075.5875 | 13768.89688 | 2.345161077 | 0.153261362 | |

| Residual | 7 | 41098.36167 | 5871.194524 | |||

| Total | 11 | 96173.94917 | ||||

| Coefficients | St Error | t Stat | P-value | Lower 95% | Upper 95% | |

| Intercept | 1028.06875 | 55.71160132 | 18.45340514 | 3.40205E-07 | 896.3317464 | 1159.805754 |

| Quarter | 12.60625 | 6.772644034 | 1.86134838 | 0.105003403 | -3.408508331 | 28.62100833 |

| summer | 66.99375 | 62.9285181 | 1.064600789 | 0.322395241 | -81.80855001 | 215.79605 |

| Fall | -4.4125 | 64.01253402 | -0.068931813 | 0.946971672 | -155.7780903 | 146.9530903 |

| Winter | 100.0145833 | 65.77954125 | 1.520451214 | 0.172202085 | -55.52931517 | 255.5584818 |

Table 9: Auditor’s expectation for 2019

| Auditor’s Expectations for 2019 Quarterly Sales Revenue of Herbalife. | |||||||

| (in million) | |||||||

| Sales revenue[hat]=1028+12.6 Quarter+67 Summer-4.41 Fall+100 Winter | |||||||

| Quarters | Quarter | Asserted | Expectation | Difference | Materiality | Materiality | Difference |

| Spring | 13 | $1,172.20 | $1,191.80 | ($19.60) | $59.59 | 5% | -1.64% |

| Summer | 14 | $1,240.10 | $1,271.40 | ($31.30) | $63.57 | 5% | -2.46% |

| Fall | 15 | $1,244.50 | $1,212.60 | $31.90 | $60.63 | 5% | 2.63% |

| Winter | 16 | – | – | – | – | 5% | – |

| Total 2015 revenue | $3,656.80 | $3,676 | ($19.00) | $183.79 | 5% | -0.52% |

Table 10: Multivariate Dummy Variables Model (some economic indices and Trend Variables)

| SUMMARY OUTPUT | ||||||

| Regression Statistics | ||||||

| Multiple R | 0.905031342 | |||||

| R Square | 0.81908173 | |||||

| Adjusted R Square | 0.715699862 | |||||

| St Error | 49.85640021 | |||||

| Observations | 12 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 4 | 78774.32467 | 19693.58117 | 7.922876048 | 0.009739544 | |

| Residual | 7 | 17399.6245 | 2485.660642 | |||

| Total | 11 | 96173.94917 | ||||

| Coefficients | St Error | t Stat | P-value | Lower 95% | Upper 95% | |

| Intercept | -8321.287557 | 2990.002918 | -2.7830366 | 0.027179224 | -15391.52097 | -1251.054144 |

| DP Income | 0.526043942 | 0.199477892 | 2.637103981 | 0.033564376 | 0.054353682 | 0.997734202 |

| Retail Sales | 0.003938329 | 0.00098293 | 4.006725368 | 0.00514569 | 0.00161407 | 0.006262588 |

| S&P 500 | 0.339442951 | 0.132128838 | 2.56903003 | 0.037060266 | 0.027007898 | 0.651878005 |

| Trend | -133.1742769 | 44.61134288 | -2.985211122 | 0.020363974 | -238.6633402 | -27.68521367 |

Table 11: Auditor’s expectation for 2019

| Auditor’s Expectations for 2019 Quarterly Sales Revenue of Herbalife. | |||||||

| (in million) | |||||||

| Sales revenue[hat]=1053+15 Quarter | |||||||

| Quarters | Quarter | Asserted | Expectation | Difference | Materiality | Materiality | Difference |

| Spring | 13 | $1,172.20 | $1,060.50 | $111.70 | $53.03 | 5% | 10.53% |

| Summer | 14 | $1,240.10 | $1,224.90 | $15.20 | $61.25 | 5% | 1.24% |

| Fall | 15 | $1,244.50 | $1,203.20 | $41.30 | $60.16 | 5% | 3.43% |

| Winter | 16 | – | – | – | – | 5% | – |

| Total 2015 revenue | $3,656.80 | $3,489 | $168.20 | $174.43 | 5% | 4.82% |

Graph 1: Quarterly sales of Herbalife (audited)

Graph 2: Auditor’s expectation for 2019

Graph 3: Auditor’s expectation for 2019

Graph 4: Auditor’s expectation for 2019

Back To News

Is Herbalife a pyramid scheme?

More Stories

Personal Branding – So What Is The Big Deal?

Three Keys of Branding That Will Turn Small Business Advertising Expense into an Investment

Perbedaan Logo Design Dengan Branding